Dutch IBAN

Within the Single Euro Payments Area (SEPA), companies and institutions are not allowed to exclude IBANs from other SEPA countries. Dutch companies and institutions may therefore not discriminate against IBANs from Malta, Hungary, or Iceland, for example, for their transfers and direct debits. The website of DNB provides more information about SEPA and IBAN discrimination. It also explains how you can report IBAN discrimination if an organization does not comply with this SEPA regulation.

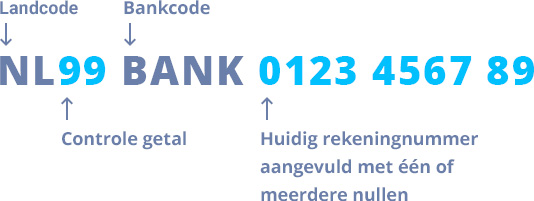

Structure of Dutch IBAN

A Dutch IBAN consists of 18 digits and letters:

- Always starts with the country code NL.

- This is followed by a 2-digit check digit. This allows a bank, company, or institution to check for any typing errors in long IBANs in its customer records.

- A 4-letter bank code or bank identifier indicates which payment service provider (which bank) issued the IBAN.

- The last 10 digits of a Dutch IBAN are determined entirely by the payment service provider that issues the IBAN. Two or more payment service providers can use the same 10 digits for an IBAN. The different four-letter bank codes of the payment service providers ensure that each IBAN remains unique.

Special features of Dutch IBANs

Issuing an IBAN for payments is not allowed without further ado. A payment service provider must have certain licenses for this. In addition, there are various laws and regulations that the payment service provider must comply with. The Dutch Payments Association publishes information for payment service providers who are considering issuing Dutch IBANs.

Below are the details for account holders of a Dutch IBAN:

-

1. Short account number

To make a transfer, the payer must agree to the recipient’s full IBAN. With some banks, the payer only needs to fill in the last few digits of a charity’s account number. Before making the payment, the bank completes this account number to form the full IBAN. This temporary service was set up when we switched from shorter account numbers of up to 10 digits to IBAN in the Netherlands. We are now used to IBAN. The IBAN of a charity can be stored in the bank’s address book. In practice, the bank hardly ever needs to use this service anymore.

-

2. Do not reissue account numbers

Since our payments accounts have IBANs, payment service providers no longer issue account numbers that previously belonged to someone else. This reduces the risk of errors. What if someone wants to transfer money to an account that has been in their address book for a long time but now belongs to someone else? A successful IBAN Name Check will reveal that the name and IBAN do not match. If a payment order is still given and the payer later wants that money back, a transfer of 1 cent can be made with a request for a refund. A second option is to write to the recipient of the money. If no name and address details are known, the payer can ask their own payment service provider for assistance. Within the Netherlands, this is usually done via the Procedure for Undue Payments. Outside the Netherlands but within SEPA, a slightly different procedure may be required, known as a ‘Request for Refund by the Originator’.

-

3. Right to an account?

The Financial Supervision Act (Wet op het financieel toezicht in Dutch) stipulates when someone is entitled to an account. The same act also stipulates when that right no longer applies. Payment service providers must always comply with the law before they are allowed to issue an account.

- If an applicant is on a European or national sanctions list, a payment service provider may not issue an account.

- Persons with a Dutch BSN who live outside the European Union do not have a legal right to a Dutch IBAN. It is up to payment service providers to determine whether and under what conditions they offer an account to persons living outside the EU. This also applies to countries outside the EU but within the European Economic Area.

- For example, is an applicant listed in the Central Guardianship and Administration Register or the External Referral Register (in Dutch)? If so, the payment service provider may impose additional conditions on the opening of a payments account.

Those who are unable to open an account through the normal application process may sometimes have to follow a different application process. Information about this can be found on the page about accounts.

-

4. Banking Information Reference Portal

The Banking Information Reference Portal is an electronic system for requesting identifying details of an account holder. Financial service providers that issue Dutch IBANs or offer safe deposit boxes are required by the Financial Supervision Act (Wet op het financieel toezicht in Dutch) to connect to the Banking Information Reference Portal. Authorized agencies can request the personal details of the account holder for any Dutch IBAN.

-

5. The Dutch Tax Administration must verify that the IBAN is correctly recorded in its records

A payment service provider must submit information about the account holder or account holders for each Dutch payments account to the Dutch Tax Administration. This ensures that the Dutch Tax Administration can verify whether a payments account is in the name of the person entitled to a refund or allowance. This prevents money from being transferred to the wrong or even fraudulent account number. The obligation for the Dutch Tax Administration to only transfer money after it has been established that the IBAN provided actually belongs to the entitled person is laid down in the single bank account measure (in Dutch).

-

6. Dutch Tax Administration to switch to a new account number for payments

One of the most commonly used account numbers in the Netherlands will be that of the Dutch Tax Administration. The national government has announced that the Dutch Tax Administration will have a different house bank from May 1, 2026. This means that there will be a new IBAN. Nothing will change until May 1, 2026. Will you receive a new account number from the Dutch Tax Administration? Make sure that this is the account number of the Dutch Tax Administration and not that of a fraudster. Check the result of the IBAN Name Check. Or wait until the Dutch Tax Administration transfers money to you. Does the same new account number appear on the message from the Dutch Tax Administration? Then you can be sure that you can use this new account number for your payment to the Dutch Tax Administration.

-

The 099 series is only for G accounts

The last 10 digits of the Dutch IBAN are determined by the payment service provider that issues the IBAN. According to the IBAN Registry, the payment service provider must take one exception into account. The series may only start with the digits ‘099’ if it is a G account of a hirer or contractor.mg

History of Dutch account numbers

An account number originally started as a short number consisting of just a few digits. In longer account numbers, a certain part was linked to a specific bank branch. There was no nation wide standard for account numbers, which made payments between banks difficult.

In 1918, the PTT introduced the Postgiro, which made it relatively easy for citizens and businesses to transfer money to each other within the Postgiro system. Postgiro accounts had an account number of variable length, without a check digit. In the 1960s, the Bankgirocentrale was introduced for all other Dutch banks, along with a standardized 9-digit account number with a check digit.

The supply of account numbers was limited and, unlike the Postgiro, was kept centrally for banks. If an account number had not been active for a number of years, a bank could reissue this account number to a new account holder.

With the introduction of SEPA in 2014, an IBAN became mandatory for all payments accounts within SEPA. The stock of available account numbers is now so large (billions of account numbers per bank) that it is no longer necessary to reissue old account numbers.